Going down: the elevator industry at risk

The maintenance model of the elevator industry, providing for 75% of its profits, is outdated and the four main OEMs are not countering the downturn.

The global elevator market is a hidden niche worth more than $90bn (source: Freedonia research), yielding massive cash-flows. The well-off elevator group of manufacturers, made up of Otis, Schindler, Thyssen and Kone has recently been shaken. Two major events happened in two months:

- Otis span off from the United Technologies conglomerate and listed on the NYSE on April 3rd,

- The elevator branch of Thyssenkrupp was sold to buyout firms Advent and Cinven for €17.2bn on February 27th, or more than 14 times its earnings of €1.2bn.

In a world hit by the COVID-19 crisis, elevator equity stocks with their countercyclical maintenance contracts — that yielded recurring profit for decades — look like a golden safe haven, don’t they? Well, not so much. We are convinced that the elevator industry faces a long-term downward trend and is struggling to realize it.

In this article, we look into:

- Why the maintenance model of the elevator industry, providing for 75% of its profits, is virtually dead.

- How the COVID-19 crisis can accelerate this downturn.

- and why the 4 main OEMs are not tackling this risk properly.

In the next article, we document how a high-technology contrarian approach can reverse the trend.

Elevator profits come from maintenance

The elevator business model is simple:

- assemble and install new elevators. These elevators have the same lifetime as the building they’re installed into;

- maintain a large installed base of elevators worldwide, as new elevators pile up on this aging and ever-growing base;

- try to grow this maintenance portfolio permanently as any maintainer can maintain almost any elevator;

- modernize the old elevators of the maintenance portfolio, selling and performing overhauls.

The maintenance portfolio is the key: its long-term contracts stay in the hands of the same maintainer for decades, provide recurring revenue, free cash flow, and long-term visibility. The key target is to grow it, for example by selling new lifts with low margins but convert these into the maintenance portfolio.

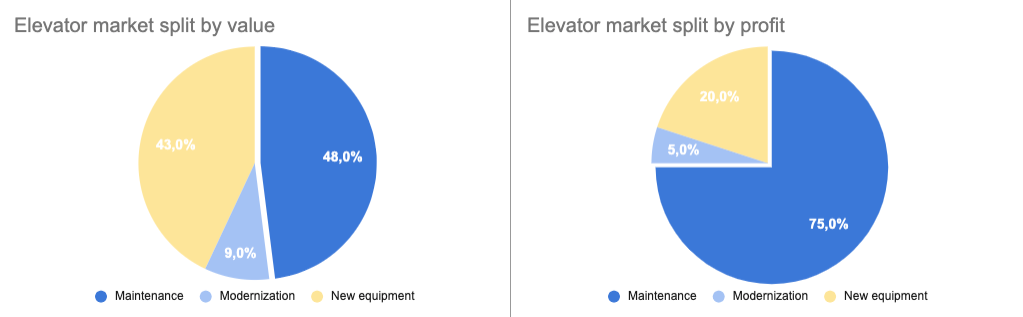

And that is why maintenance accounts for 48% of the total industry sales and… 75% of its profits.

Source: Credit Suisse public Schindler primer, 2017

However, growing the portfolio is precisely where the OEMs fail at their mission. They fail for a simple reason: the current maintenance model is outdated and underperforming.

Elevator maintenance is a Means vs. Ends model

Elevator maintenance contracts were born in the first part of the previous century, as a widespread model to service the installed base of elevators under constant terms. For safety purposes, most countries adopted elevator maintenance regulations that rely on the same components:

- maintenance contracts with an entitled company are mandatory;

- they should provide for a minimum of 1 to 12 maintenance visits per year;

- third-party inspections are mandatory on a yearly or multi-year basis.

The four OEMs built their service business model around those regulations:

- Provide a maintenance contract that enforces those mandatory visits and include emergency breakdown response

- Sell additional repairs on top of the contract: spare-parts, specific breakdown repairs.

The sum of all those contracts is the maintenance portfolio of the OEM, that drives their recurring revenue, profits, and market cap.

The clients, property owners or managers, therefore purchase means (visits and breakdown response), and not results (guarantee that the elevator works). Elevators are a complete black box to them.

This system is what we call the Means model of elevator maintenance.

The flaws of the Means model entail competition from lower-end players

When you sell means, you focus on productivity, not on outcomes for the customer. The two drivers of productivity for an elevator maintenance portfolio are density and labor efficiency. Thus, on average, each elevator technician that maintained 80 units in the last decade now has over 120 to look after.

Reducing maintenance visits to the minimum safety regulatory requirements achieved such labor productivity gains. Then what? Elevators start to break down. Often. In Europe, the average breakdown rate is 5 per year per lift. Sometimes, very often. An investigation from NY1 found that New York City’s 3,200 public housing elevators had more than 44,000 outages in 2018, averaging to about 14 breakdowns per year per elevator. A New York University study said the New York City’s metro elevators had, on average, 53 failures per year.

Are breakdowns a problem? Not much in the short term: they encourage higher repair sales.

However, they also trigger a long-term trend of local independent service providers that focus on bridging this quality gap, at least partially.

By offering simpler terms, lower prices, and a direct line to the owner, SMEs win over contracts from the OEMs and eat into their installed based. Maintenance contracts prices are going down, margins are getting under pressure, and churn increases.

OEMs barely compensate this trend by converting new equipment installations into the maintenance portfolio, and by acquiring those small and mid-sized competitors.

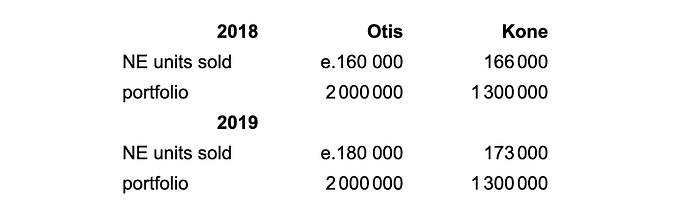

Let’s look at the market leader, Otis, and its fast-growing challenger, Kone, figures.

Otis data comes from UTX annual reports. New equipment Otis units are estimates, using their market share (±20%). Kone data comes from their annual reports.

Both Otis and Kone’s maintenance portfolios are flat, although they install 150–180k elevators every year.

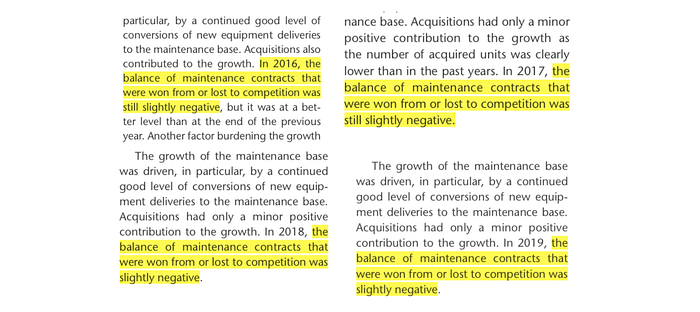

Kone provides more details in its investor reporting: “In 2019, the balance of maintenance contracts that were won from or lost to competition was slightly negative”, a sentence used in each annual report, every year since at least 2015.

What is the actual organic (excluding new equipment and acquisitions) erosion rate? Kone gives us the following data: 50% conversion of their China new equipment units and 80% conversion elsewhere, 90% retention of their portfolio (10% churn). If we kindly estimate that Kone’s portfolio grows by ±50k units per year instead of being flat, at best, we calculate a yearly organic churn of -64k units, or -4.9%.

As Kone is thought to be the best in class, this trend is likely to be similar if not worse for the other three OEMs. Local players gradually take over their installed base. Furthermore, with competition driving prices downwards, their portfolio total value might even be decreasing, even though the total of elevators maintained is flat or slightly growing.

Quality, not price, drives churn

Whether in office, housing, or public buildings, all surveys always end up putting HVAC/Heating and Elevators in their top 3 pain points.

As the CEO of a €14bn commercial real estate company in Paris once told me: “Temperature is a subjective feeling. Some feel well at 18°C while others only at 22°C. Elevator annoyance is always objective: they work, or they don’t. And they often don’t.”

We calculated that the approximate downtime of an elevator in France is eight days per year. France is not the country with the most breakdowns: a 2010 IBM Smart Buildings study showed that NYC office workers spent a total of 5.9 years stuck in elevators.

According to Credit Suisse, the average maintenance contract price per elevator is slightly over €2000 worldwide, ranging from €900 in China to €4000 in the US. An office building operating costs in the US, excluding real-estate taxes, ranges from $8 per square foot to $12 per square foot, says the BOMA International 2020 Office Market study.

In other words, elevator maintenance accounts for only 2.5 to 5% of a building’s operating costs but systematically ranks in the top 3 of their pain points.

The housing segment is no different: in Paris, an elevator contract averages €66 per flat per year, e.g. only 5% of the operating costs, but still a top 3 inconvenience. There is a major service quality issue everywhere elevators are used.

Despite my statement in the subtitle, prices also sometimes drive churn. In EMEA and the Americas, more than half of the installed elevators are >20 years old. Their contracts have an automatic price indexing formula, growing 1–3% per annum. Some customers can end up paying prices 2x — 3x the current average market quote. Such contracts are usually terminated for price reasons. It frequently happened in the aftermath of the 2008 crisis, but today the ‘excessive price’ surplus is almost dry. Today, churn is mostly motivated by poor quality, with breakdowns and service problems getting on the nerves of property owners and managers.

From a final customer point of view, it is really quite simple: nobody cares about elevators until they are not working.

In EMEA, we estimate that there are continuously ±20% of unhappy customers, facing excessive downtime or poor service from their maintainer. We are convinced this is driving the structural 5% yearly churn of the four OEMs to SMEs. We think of this 20% of customers not as a finite base but rather as a flywheel: the combined effect of an aging elevator base and an outdated model will make almost every customer unhappy enough to consider churn at least once in a decade.

But whom to turn to? Every company offers the same means model. Only SMEs have the light differentiating claim of being closer to customers. Hence, most companies only differentiate through price. Customers, not being able to compare two offers, go for the cheapest.

That is how the means model, generating poorer and poorer quality of service, yields structural churn, and a portfolio value decrease year after year.

A softening regulation towards less mandatory visits will accelerate the downward trend

Industry experts in geographies where the number of required visits is high are expecting a loosening trend in regulation in the coming years. The politics are easy: standardize policy (e.g., in Europe), encourage price decrease — especially for public housing. As soon as the decrease of required visits won’t be associated with lower safety conditions, the reforms will happen.

This can happen soon. When benchmarking markets today, we observe this:

- the lower the visit requirements, the lower the breakdowns;

- e.g., in Northern Europe, Swedish regulation only requires yearly third-party inspections and no maintenance visits. Market practice is four maintenance visits per year and there are <2 breakdowns per year.

- The higher the visits requirements, the higher the failures: France has 9 inspections per year, Spain and New York have 12. In these geographies, the breakdown rate is ≥5.

The productivity-driven current model works like this: the more a technician needs to do (mostly useless) frequent checks, the less real maintenance checks are performed, the more failures occur. Analysis of the safety incidents per geography should show the same trend. Hence, we do not see a correlation between a higher frequency of checks and a lower rate of incidents. In fact, we rather see the opposite.

In a means-rather-than-results model, what happens when the means sold are reduced? The prices go down. Without a strong differentiator to justify the value-add, fewer visits will automatically mean lower prices in the elevator maintenance market. Customers will still not be able to differentiate an offer from the other, will churn to another provider in the hope of a change, and pick a cheaper contract in the process. Why wouldn’t they?

Elevator maintenance is based on a means model sustained by regulation. As this regulation could loosen in the years to come, the trend in decreasing portfolio value could accelerate further.

The COVID-19 crisis will accelerate the model’s downturn

The COVID-19 crisis adds two impacts: halts in new equipment installations and an increased pressure to reduce the number of yearly visits.

According to Credit Suisse, the elevator market was down 2% in 2009 and 2010. Maintenance portfolios were mostly stable per their countercyclical nature. It was new equipment installations and refurbishments of existing elevators that stopped.

The COVID-19 crisis will make this worse. The construction sector was put to an almost full stop in countries under lockdown (more than half of the world’s population as per Euronews count on April 3rd). The OECD predicts a -2% contraction in GDP per month of confinement. Less new installations means less additions to the maintenance portfolio.

In addition, the crisis might also accelerate the change in the number of visits performed per elevator. Most elderly homes in France have asked their service providers not to come to perform the maintenance visits. This trend could endure in post-confinement societies, where the sanitary balance will be fragile until a cure or vaccine is found.

The OEMs could watch their portfolio going from flat to worse, handing over the old elevator base to local service providers at a faster pace than anticipated.

Are the OEMs tackling this risk? Product innovation won’t move the needle

How do OEMs react to such a threat? How to create portfolio growth again? The multinationals are rightly looking at innovation. As often, incumbents are doing it the wrong way. This proves to be a case-in-point innovator’s dilemma: short-term fear of further weakening the maintenance model, in conjonction with huge cultural gaps, undermine innovation efforts.

Let’s look at the product innovation angle to secure the service contracts of new elevators, with those two flagship initiatives: Thyssenkrupp MULTI and Kone DX.

“MULTI, the world’s first rope-free lift. By moving multiple cars in a single shaft vertically and horizontally, MULTI opens the door to new possibilities — in all directions!” says Thyssenkrupp’s website. This new technology was announced in November 2014 and is currently tested in their research center. Will it impact the service model in the next two decades and discourage third-party competitors? No. Even if the high-rise segment is growing (note: according to the Council on Tall Buildings and Urban Habitat (CTBUH), 146 buildings of at least 200 meters were completed in 2018, more than twice the 2010 figure). It will represent a fraction of newly installed elevators, and therefore of the total installed base.

If not high-rise high-tech, then what about bringing digitalization to all new elevators? Could it create customer value-add in the long term and have the effect of discouraging maintenance by third-parties? “KONE DX Class elevators redefine the elevator experience with built-in connectivity for improved people flow — helping to create an experience that connects on every level.” says their website. What could that mean? Looking into details and at the promotional video, Kone’s offer englobes in-cabin screens, connexion to room-service robots to let them use the elevators in a hotel, building access tools, or… music in the elevator cabin.

The idea of an advertising in-cabin screen has been around for decades without ever proving its concept. At 1m/s, a trip of 6 floors is done in 18 seconds. Just enough to get-in, feel awkward if there is someone else or look at yourself in the mirror and get out. In-cabin screens are a nice-to-have feature, not a business revolution. The innovation leader, Captivate Network, a startup founded in 1997, has today 11 600 connected screens in 1 600 buildings. It was sold to Gannett Co. Inc. in 2004 for an undisclosed amount; however, the four main acquisitions by Gannett this year were reported for a total cost of $169M (p.20).

If getting the end-user’s eyeballs doesn’t seem compelling, could an elevator with more electronics, digitally connected to its manufacturer 24/7 be an advantage against third-party maintainers? We witnessed this effect with the machine-roomless elevator launched by Kone in 1996. As the automotive industry has demonstrated, adding new components and software is a service advantage and protects your product from being serviced by someone else. Adding 24/7 internet connectivity and native remote monitoring should add a layer to the OEMs’ defensive differentiation.

But what is the real business impact? Nowadays, machine-roomless elevators can be maintained by any local independent SME. The protection induced by new product development is efficient for 5 to 10 years, the “time-to-maintain” span for any service provider. Moreover, local regulation is now easing the change of service providers. In 2012 a French decree imposed manufacturers to hand over any necessary tool, password, code, documentation to any new maintainer. What we can thus expect from new digital-native elevators is an increase in conversions in non-China geographies and an increase in retention during the first years. If we take back the Kone figures and make aggressive assumptions, it would translate into:

- an increase of 10% in conversion for non-China installations, from 80% to 90%

- an increase of 1% in overall retention of the total portfolio, from 90% to 91%

we land on a total growth of 70k units instead of the estimated 50k, and on an organic erosion of -3.9% instead of -4.9%, still handing over tons of value to independent local companies.

Retrofit innovation is key to win the battle.

For OEMs, new elevator product innovation is a necessary and defensive move, but it will be far from enough to stop the downturn. And what we know is that the big four OEMs, as any worldwide manufacturer, have no retrofit innovation culture.

Predictive maintenance seems to be stuck at the marketing stage

In 2015, Thyssenkrupp Elevator announced its predictive maintenance initiative, MAX. It was based on a partnership with Microsoft and supposed to reduce downtime of elevators by up to 50%. Ambitions were high: “MAX is a major milestone in ThyssenKrupp Elevator’s business strategy. In the 18-month launch period the company aims to connect some 180,000 units in North America and Europe[…]. In two years, the offering will be expanded to all continents, becoming available to some 80% of all elevators worldwide”.

More than four years later, they connected 128,000 elevator units (Jan. 2020 figure) out of their 1.4m elevators portfolio. This figure is much less than their new elevators installed during the same period (approx. 280k in four years). Does it mean that not every elevator can be equipped with MAX? A 2019 press release on a new maintenance deal with EDF seems to confirm it. Out of 585 elevators serviced, only 17 of them have been announced to be equipped with MAX. But if predictive maintenance reduces your operational costs and churn, why not roll it out widely?

Has their MAX initiative been able to reverse the organic erosion of their portfolio? Not if we look at their Elevator Technology Company Presentation released in January for investors, available here (under the Elevator Technology Day section). They claim a high global conversion rate of 70–80%, new equipment units per year growing from 60k units to 85k from 2012 to 2019, but a portfolio growing only 40k units per year on average for the same period. There is no visible acceleration in recent years, as 2018 and 2019 portfolio figures are shown flat at 1.4m. The retention rate claimed is the same as Kone’s, 90% — in other words, a 10% churn. Did MAX deliver clear KPIs, such as a strong reduction in breakdowns or operating costs? Even if it did, until this is not reflected in portfolio growth, the point is missed.

Then what is wrong?

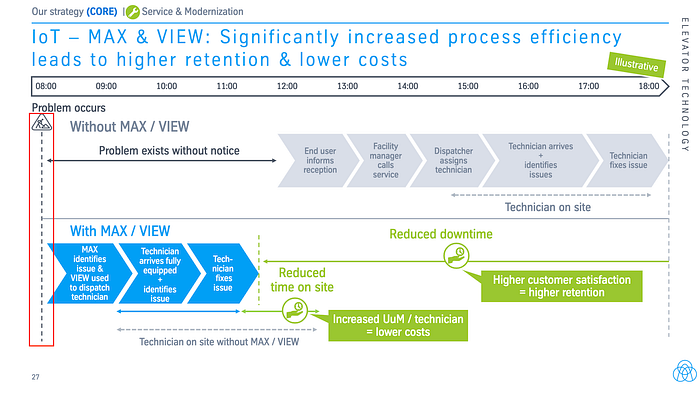

MAX does not answer the root of the service quality problem: the means model. It just enhances it. Does its predictive technology avoid breakdowns? It rather seems it allows a faster response time. OEMs are building technology on the wrong product vision.

This slide is from the same public company presentation. What are we looking at? In both cases, with MAX or without it, a problem occurs. The only difference is that the customer does not need to call Thyssen to report it; Thyssen can notice it first. Manufacturers have been able to do something similar on their electronics for decades, as early as with the OTIS Remote Elevator Monitoring system (REM) introduced in the 1980s. The downtime reduction is not theoretically achieved by reducing the breakdown rate, but by a more prompt response.

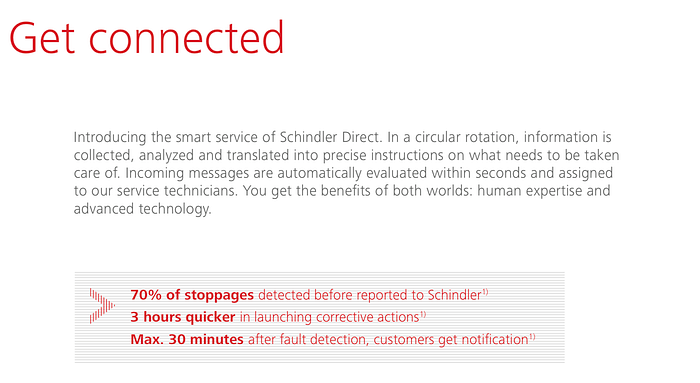

This image is a part of the Schindler Direct brochure, their predictive maintenance initiative (available here). Similar conclusions: the KPIs shown, reported on a test on 3,000 elevators demonstrate faster response times, not a reduction in breakdown rate. This technology also seems to work only on new Schindler units: “New Schindler elevators and escalators are ready with Schindler Direct” says the brochure regarding compatibility.

OEMs are executing the wrong product vision not by purpose, but for cultural reasons. As manufacturers, their innovation and research culture is rooted in their factories.

The service retrofit environment of various makes, ages, conditions, and components is a non-technological, non-mathematical world for them. Solving it is delegated to their service technicians. They live by the undocumented knowledge of a dispatched workforce.

“It definitely needs a cultural change because a company like Thyssenkrupp is more a classic engineering company.” said to the Wall Street Journal Reinhold Achatz, Thyssenkrupp’s chief technology officer in October 2019, discussing AI and predictive maintenance.

A high-tech contrarian move reverses the trend

If elevators maintenance is the core of the industry profits and market caps, if its growth machine is threatened by commoditization and if the industry leaders are not tackling the risk properly, what would?

Real predictive maintenance, aimed at creating value for the customer instead of perpetuating an outdated model, will disrupt the industry.

We document in detail this opportunity in a second article available here, detailing uptime’s vision.